We doubled our referral bonus!

We doubled our referral bonus!Ready to build a better future? Apply now.

Personal loansHow much of a difference can it make to choose one kind of loan over another? A huge difference. Read Laura’s story about her possible choice of payday or an installment loan to find out.

Laura lives with her husband and kids in Departamento 15, an area known as “El corredor salvadoreño” in Los Angeles. She and her husband have run a Salvadoran grocery store for two years and she loves her family business. She brags about the food of her country, which she sells in her store, and her friendly smile makes her customers feel like the store is their home. You wouldn’t guess by looking at her, but she wakes up every day (even Sundays) at 5:30 am to open the store and doesn’t close till 8 pm. She and her husband work very hard and do everything themselves.

Typically, they earn about $400 per month that they can put toward having a nice life in the US and to send money to family back in El Salvador. Some months, they even add to their savings for unexpected emergencies, like the one that finally happened. Laura’s husband got sick and spent two whole weeks at the hospital. On top of the emotional stress and having to deal with the grocery store on her own, Laura needed an extra $1,000 more than their savings to cover her husband’s medicine and care when he finally came home.

The rest of their family lives in El Salvador and wouldn’t be able to help, so she considered a loan.

Laura has never had a credit card or other type of loan before, so she didn’t have any credit history. She learned that her options were limited to payday, installment, pawn, or auto-title. Laura saw many payday and title loan lenders in her neighborhood. Unwilling to give up or risk anything of value, especially their car, she compared loans from a payday lender and an installment loan from Oportun.

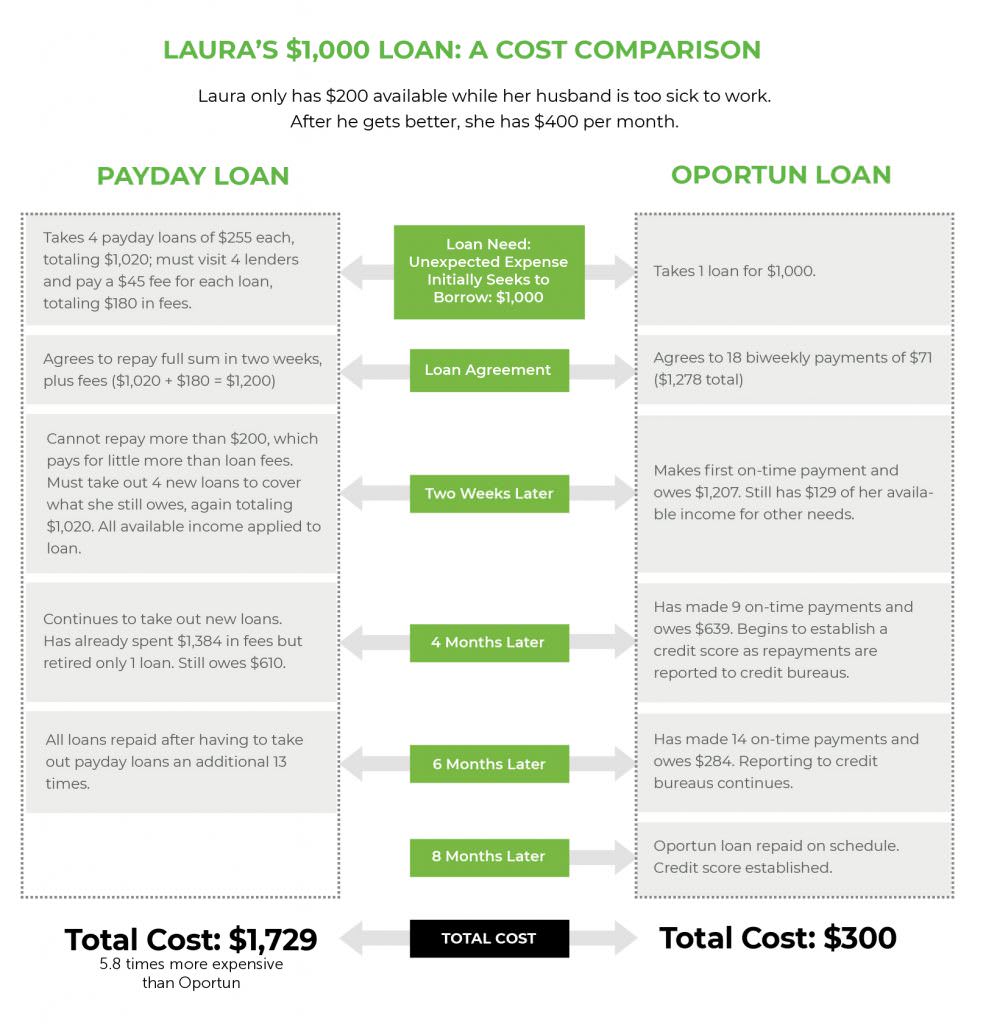

If Laura chose a payday loan…

California law restricts payday loans to $255 and allows a $45 fee on each loan. Each lender can only make one loan per person. Laura had to take out 4 loans from 4 different lenders, each with a $45 fee, to get $1,020 in cash. She was relieved though, because she was able to get the money the same day she applied. Her husband wouldn’t miss a single dose of his expensive medications!

Loan Example: Laura needed $1,000

$255 x 4 loans = $1,020

$45 x 4 loans = $180 in fees

APR: about 459%

The payday loan contracts required Laura to repay the entire $1,020 + fees in only two weeks. This would have been difficult under the best of circumstances but was especially tough while her husband was still recovering. In addition to looking after him, she need to look after her kids, so she had to make the difficult choice to close the store early several evenings and even one whole weekend. Money was tight.

On the due date, Laura only had $200 to spare to cover loan payments, which only covered the fees. She had to take out four new loans (from another four lenders) to pay the original loans off. These came with another $180 in fees again.

It’s been four months now. Laura’s husband is doing much better. The grocery store is open all the time and they’re back to making around $400 per month for flexible spending. However, it’s all going toward their payday loans. Laura has only been able to pay off one so far. They’ve not sent any money to family for months, and money feels very tight at home. She’s had to roll over eight more times, paying a fee for each new loan. Her total fees so far add up to $1,384, which doesn’t include the borrowed amount. Her husband is finally well enough that he’s looking for short-term work that can help pay off the loans.

If Laura chose an installment loan with Oportun…

Laura had heard that California law caps interest rates on installment loans under $2,500, which make them more affordable than payday loans and she did not have to repay the loan right away. She brought her income and other required documents to one of the Oportun locations nearby (there are four within a couple miles of the “El corridor salvadorno” in Los Angeles). Upon approval, she was able to receive the $1,000 she needed the very same day she applied and did not have to give her car title or any collateral. She was thrilled that her husband would be able to come home from the hospital with everything that he needed.

Laura’s loan contract required her to repay the loan and interest in installments (fixed, equal payments spread over a period of time). For example, she could borrower the whole $1,000 and pay $71 every two weeks for 18 payments (8 months), totaling $1,278.

Loan example: Laura needed $1,000

$71 x 18 payments = $1,278

APR: 56.5%

The first week her husband was out of the hospital, Laura closed the store early a few evenings and for an entire weekend to care for him and the children. She earned less money in their business because of it, but had $200 extra after paying her bills. Since Laura only needed $71 for the first loan payment, she sent some funds to family in El Salvador, and some went to school supplies for their kids.

Finally, her husband recovered and was able to help in the store again. It’s been four months, and Laura has made nine, on-time and complete payments. She still owes $850, but the payment schedule feels realistic. They are able to take care of their needs, including helping their family in their home country. They plan to pay off the loan in 18 payments, as scheduled.

But here’s the final surprise… and the happy ending: Oportun reported Laura’s account and good payment history to two of the major credit bureaus in the United States. That means Laura is on her way to establishing the kind of credit history and score that could qualify her for other possibilities in the future, like traditional loans or credit cards, should the need arise.

And now you know why Oportun describes its offering as “loans for a better future.”

Which ending do you prefer?

The information in this site, including any third-party content and opinions, is for educational purposes only and should not be relied upon as legal, tax, or financial advice or to indicate the availability or suitability of any Oportun product or service to your unique circumstances. Contact your independent financial advisor for advice on your personal situation.

Personal loans through Oportun subject to credit approval. Terms may vary by applicant and state and are subject to change. If you refinance, you may pay interest over a longer period of time or at a higher rate and the overall cost of your loan may be higher. Loans in NM and WI are originated by Oportun, Inc. California loans made pursuant to a California Financing Law license. NV loans originated by Oportun, LLC. In AL, AK, AR, AZ, CA, DE, FL, GA, HI, ID, IL, IN, KS, KY, LA, MI, MN, MO, MS, MT, NC, ND, NE, NH, NJ, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, VA, VT, WA and WY loans are originated by Pathward®, N.A.. Terms, conditions, and state restrictions apply.

You might also like